SavvyMoney

SavvyMoney Credit Score FAQs

WEA Credit Union's SavvyMoney Credit Score is available through online and mobile banking. SavvyMoney Credit Score is a free service offered to help you understand your credit score, give access to your full credit report, provide credit monitoring alerts, simulate and learn ways to improve your score and see ways you can save money on new and existing loans.

Q: What is SavvyMoney Credit Score?

A: SavvyMoney is a comprehensive Credit Score program offered by WEA Credit Union, that helps you stay on top of your credit. You get your latest credit score and report, an understanding of key factors that impact the score, and can see the most up-to-date offers that can help reduce your interest costs or lower your monthly payments. With this program, you always know where you stand with your credit and how your financial institution can help save you money. Credit Score also monitors your credit report daily and informs you through digital banking and by email if there are any big changes detected such as: a new account being opened, a change in address or employment, a delinquency has been reported or an inquiry has been made. Monitoring helps users keep an eye out for identity theft.

Q: What is SavvyMoney Credit Report?

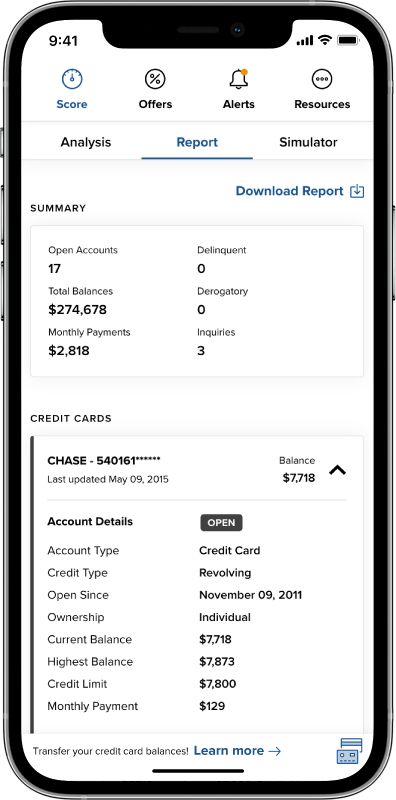

A: SavvyMoney Credit Report provides you all the information you would find on your credit file including a list of current or previous loans, accounts and credit inquiries. You will also be able to see details on your payment history, credit utilization and public records that show up on your account. Like Credit Score, when you check your credit report, there will be no impact to your score.

Q: What is the Score Simulator tool?

A: The Score Simulator is an interactive tool that allows you to select various actions you may take and see how your score could be affected. Different actions, like paying off a credit card balance might make your score move up or down. Just like checking your credit score through SavvyMoney, using the simulator does not affect your actual credit score.

Q: Is there a fee?

A: No. SavvyMoney is entirely free, and no credit card information is required to register.

Q: How often is my credit score updated?

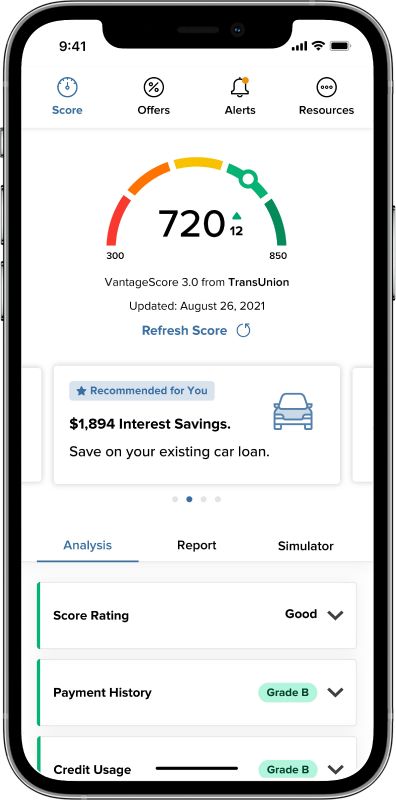

A: As long as you regularly access digital banking, your credit score will be updated every 30-days and displayed within your online banking screen. You also have the ability to refresh your credit score and full credit report every 24-hours by clicking "Refresh Score" by navigating to the detailed Credit Score Dashboard from within digital banking.

Q. How does the SavvyMoney Credit Score differ from other credit scoring offerings?

A: SavvyMoney pulls your credit profile from TransUnion, one of the three major credit reporting bureaus, and uses VantageScore 3.0, a credit scoring model developed collaboratively by the three major credit bureaus: Equifax, Experian, and TransUnion. This model seeks to make score information more uniform between the three bureaus to provide consumers a better picture of their credit health.

Q: Why do credit scores differ?

A: There are three major credit-reporting bureaus—Equifax, Experian and Transunion—and two scoring models—FICO or VantageScore—that determine credit scores. Financial institutions use different bureaus, as well as their own scoring models. Over 200 factors of a credit report may be considered when calculating a score and each model may weigh credit factors differently, so no scoring model is completely identical but should directionally be similar.

Q: Will WEA Credit Union use SavvyMoney Credit Score to make loan decisions?

A: No, WEA Credit Union uses its own lending criteria when making final loan decisions. However, the SavvyMoney tool can show you estimated savings opportunities on new and existing loans. Final rate, term, monthly payment, and other factors will be determined at the time of application.

Q: Will SavvyMoney share my credit score with WEA Credit Union?

A: No, WEA Credit Union does not have access to your credit file unless you choose to share with them. However, if you would like to share your credit report with your financial institution or any trusted party, you can easily download your SavvyMoney credit report by navigating to the "Credit Report" tab and clicking "Download Report".

Q: How does SavvyMoney Credit Score keep my financial information secure?

A: SavvyMoney uses bank-level encryption and security measures to keep your data safe and secure. Your personal information is never shared with or sold to a third party.

Q: If the financial institution doesn't use SavvyMoney Credit Score to make loan decisions, why do we offer it?

A: SavvyMoney Credit Score can help you manage your credit so when it comes time to borrow for a big-ticket purchase—like buying a home, car or paying for college—you have a clear picture of your credit health and can qualify for the lowest possible interest rate. You'll also see offers on how you can save money on your new and existing loans with ABC financial institution.

Q: What if the information provided by SavvyMoney Credit Score appears to be wrong or inaccurate?

A: The SavvyMoney Credit Score makes its best effort to show you the most relevant information from your credit report. If you think that some of the information is wrong or inaccurate, we encourage you to take advantage of obtaining free credit reports from www.annualcreditreport.com, and then pursuing with each bureau individually. Each bureau has its own process for correcting inaccurate information but every user can "File a Dispute" by clicking on the "Dispute" link within their SavvyMoney Credit Report. However, The Federal Trade Commission website offers step-by-step instructions on how to contact the bureaus and correct errors.

Q: There is a section on the site that features both WEA Credit Union product offers and financial education articles. Why am I seeing this?

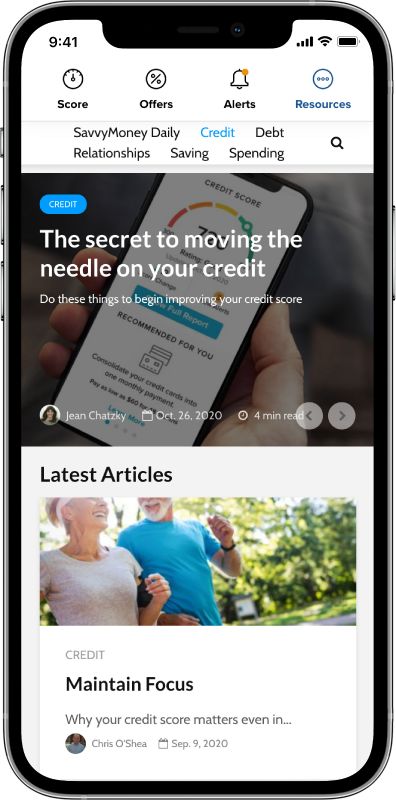

A: Based on your SavvyMoney Credit Score information, you may receive WEA Credit Union pre-qualified offers (invitation to apply) on products that may be of interest to you. In most cases, these offers may have lower interest rates than the products you already have or can save you money on your monthly payments. The educational articles, written by Jean Chatzky and the SavvyMoney team, are designed to provide helpful tips on how you can manage credit and debt wisely.

Q: Will accessing SavvyMoney Credit Score 'ping' my credit and potentially lower my credit score?

A: No. Checking SavvyMoney Credit Score is always a "soft inquiry", which does not affect your credit score. Typically, lenders use 'hard inquiries' to make decisions about your credit worthiness when you apply for loans.

Q: Does SavvyMoney offer credit report monitoring as well?

A: Yes. After you have enrolled in Credit Score for the first time, SavvyMoney will monitor and send email alerts when there's been a change to your credit profile. When applicable, you can also find these monitoring alerts within your online or mobile banking account.

Q: How do I change my email address or other personal information?

A: If you access SavvyMoney program through your online banking, you are all set and no further action is required from you! Your email address will get updated automatically in SavvyMoney when you update it within online or mobile banking. We always encourage you to inform your financial institution of any contact information updates. If you signed up with SavvyMoney from our website, please log into the website and navigate to the "Profile Settings" section under "Resources" within the tool.

Q: Am I able to choose which emails I receive from SavvyMoney?

A: Yes, you can easily choose when SavvyMoney contacts you. Navigate to the "Resources" tab and then under "Profile Settings" you can choose which email notifications you receive. SavvyMoney sends out three types of emails: Credit Monitoring Alerts, General Messages and Monthly Notices. You will be automatically enrolled in all email communications and can easily unselect the specific email types you wish to not receive.

Q: Can people use SavvyMoney on mobile devices?

A: Yes, SavvyMoney Credit Score and all other features are available on mobile and tablet devices and is integrated within our mobile banking app.